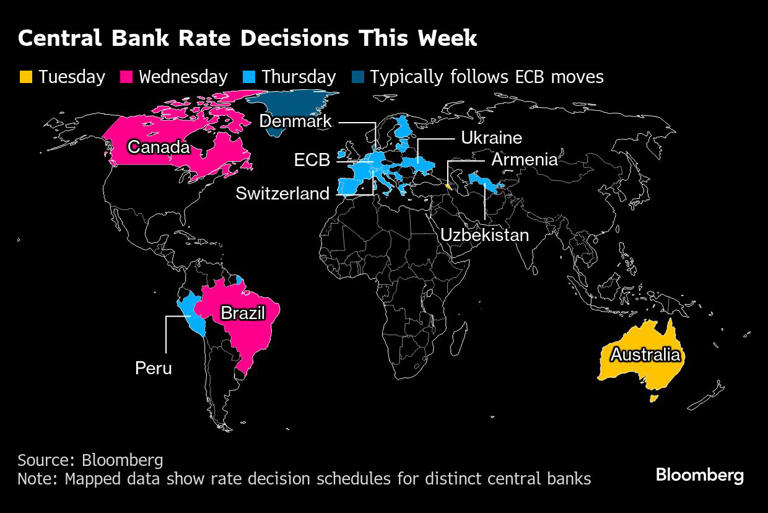

Central banks on four continents will make a final flurry of changes to borrowing costs in the coming week, before Donald Trump’s return to the White House raises the prospect of global trade turmoil.

By the time policymakers from Australia, Canada, Brazil and the euro zone convene for their first scheduled meetings of 2025, the US president-elect will have taken office, and a potential wave of tariffs could be closer to reality.

The impending change in America will help cement a particularly unsynchronized phase in monetary policy, as various economies contend with different inflation risks.

Australian policymakers are likely to keep interest rates on hold again on Tuesday, while their Canadian peers, wary of the disruption to trade that might quickly materialize from over the border, may deliver another reduction of as much as half a percentage point the following day.

In Brazil, whose currency was hit in the past week by Trump’s threat to impose tariffs on the BRICS bloc, officials are poised to jack up borrowing costs to quell surging inflation pressures.

And for euro-zone officials setting rates on Thursday, the focus is shifting rapidly from monitoring lingering consumer-price risks to worrying about the fallout from the potential hit to global commerce. ECB President Christine Lagarde and her colleagues are set to cut by a quarter point — as are the Swiss, whose currency attracts speculators at times of geopolitical stress.

Those decisions are among the highlights in a period of concentrated monetary policy action leading up to the Federal Reserve decision on Dec. 18 that economists reckon could prompt another quarter-point cut in the US.

What Bloomberg Economics Says:

“The ECB is highly likely to lower rates by 25 bps at its next meeting on Dec. 12 and members of the Governing Council are drawing battle-lines for what will follow in 2025.”

— David Powell, senior economist. For full analysis, click here

Elsewhere, US inflation and UK growth data will be among the highlights. Click here for what happened in the past week, and below is our wrap of what’s coming up in the global economy.

US and Canada

Several inflation reports, including consumer price index data on Wednesday, will offer Fed policymakers a final look at the pricing environment ahead of their meeting the following week. Any indication that progress has stalled on the inflation front could well undercut the chances of a third straight reduction in rates.

The closely watched jobs report on Friday showed the opposite: traders piled on more bets that Fed officials will lower rates another 25 basis points after an unexpected uptick in the US unemployment rate.

However, the median projection in a Bloomberg survey of economists calls for a fourth consecutive 0.3% month-over-month increase in the November core CPI, which excludes food and energy for a better snapshot of underlying inflation. On an annual basis, the core measure probably rose 3.3% for a third month.

Meanwhile, a gauge of prices paid to producers minus food and fuel probably rose by 3.2% in November from a year earlier, the biggest annual increase since June, indicating a gradual pickup in wholesale inflation.

Further north, markets and economists are leaning toward a second consecutive 50 basis-point cut from the Bank of Canada after the unemployment rate surged to its highest in three years.

The central bank’s series of cuts since June appear to have reignited the housing market and consumer spending — and Prime Minister Justin Trudeau’s plan to temporarily waive sales taxes on a variety of items has the potential to supercharge holiday shopping.

But Trump’s threat of 25% tariffs is casting a shadow over the Canadian economy, and Governor Tiff Macklem is likely to face a barrage of questions on how the uncertainty will affect the central bank’s forecasts for the coming year.

Asia

Data on Monday may show that China’s price trends improved by the thinnest of margins in November, with consumer inflation seen picking up a tad to 0.5% and the decline in factory-gate prices moderating a smidgen, in data expected to confirm that the impact from stimulus isn’t yet rippling broadly through the economy.

The following day, China gets trade data that’s forecast to show export growth decelerated last month. The Central Economic Work Conference, a meeting to determine the policy path for the country, is said to be taking place on Wednesday and Thursday.

Japan releases revised third-quarter gross domestic product data that may get a little bump from the inclusion of capital spending figures, and the Bank of Japan’s Tankan survey on Friday will indicate whether businesses remain optimistic even after the steepest quarter-on-quarter dip in profits in more than two years.

Australia publishes the NAB Business Confidence gauge on Tuesday and labor statistics two days later.

India releases consumer inflation on Thursday, and trade figures are due during the week from China, India, Taiwan and the Philippines.

Among central banks, the Reserve Bank of Australia is expected to hold rates steady on Tuesday as banks, including ANZ, push back their expected timelines for a pivot to easing. RBA Deputy Chair Andrew Hauser delivers a speech the next day.

Uzbekistan’s central bank decides on Thursday whether to hold its benchmark at 13.50% for a fourth straight meeting.

Several monetary policy decisions are scheduled for Thursday:

Among data highlights in the euro region, industrial production will be released on Friday.

Outside the currency zone, Norway and Denmark will publish inflation data on Tuesday, and Sweden will release monthly GDP numbers the same day.

In the UK, growth data are scheduled for Friday, which may show a return to modest expansion at the beginning of the final quarter. Bank of England inflation expectations are also on the calendar.

Turning south, South Africa from Monday through Thursday hosts its first meetings as the revolving head of the G-20 — taking over from Brazil — amid a deeply polarized world and a Trump presidency that’s expected to rattle global trade. Sherpas, deputy finance ministers and deputy central bank governors will gather to start laying the foundation for the presidents’ meeting next November.

In Egypt on Tuesday, data will probably show inflation slowed slightly from October’s year-on-year 26.5%. Most analysts doubt it will decelerate quickly enough for the central bank to begin a cycle of rate cuts until around March.

On Wednesday, South Africa’s inflation rate is expected to climb for the first time in nine months, to 3.1% in November from 2.8% in October, on the back of a weaker rand and rising gasoline prices.

In Russia on Wednesday, monetary policymakers will look for further signs of slowing inflation in November data, after it eased to 8.5% the previous month. That’s as pressure builds for the central bank to hike its key rate again this month in an ongoing effort to bring price growth to the 4% target next year.

Latin America

In Brazil, rising and above-target consumer prices and rates should weigh on GDP-proxy and retail sales reports.

At the same time, inflation last month probably drifted further above the 4.5% top of the target range, and the central bank is likely to see off 2024 with a rate hike of at least 75 basis points.

Central bank surveys of expectations are on tap from Brazil, Colombia and Chile, with the latter serving up market readouts from both analysts and traders.

In Mexico, October industrial production and November’s consumer price report should provide fresh evidence that Latin America’s No. 2 economy is cooling off.

Analysts expect headline inflation and the core print to both grind lower, likely green-lighting Banxico for a fourth straight rate cut at its December meeting.

Peru’s central bank is likely to stand pat and keep its key rate at 5% after November’s pickup in consumer prices.

Argentina’s economy has likely pulled out of recession and the end of capital controls in 2025 appears to be a given.

But monthly disinflation may have hit a near-term floor with October’s 2.7% reading, even as the November year-on-year reading declines for a seventh straight month.

With assistance from Patrick Donahue, Brian Fowler, Vince Golle, Tony Halpin, Robert Jameson, Laura Dhillon Kane, Monique Vanek and Paul Wallace.

This article was generated from an automated news agency feed without modifications to text.